Detroit City Snapshot

Manufacturing—particularly specialized, small-batch production—benefits from being in cities. And cities benefit from manufacturing. Firms get to tap a rich labor market as well as dense and often sophisticated consumer markets for their finished goods. Increasingly, cities see this emerging sector as rich with possibility for promoting entrepreneurship, innovation, and economic growth. But members of the Urban Manufacturing Alliance (UMA), including many city decision makers, told us they know remarkably little about smaller scale manufacturers. These innovative businesses often combine design, art, and production. As a result, they often do not fall neatly into the data collection categories that government has used to classify manufacturers for generations. What’s more, the data that do exist are often at the metropolitan level, which can swamp nuances as this sector grows and establishes itself in modest-sized clusters at the hearts of cities. The result is a dearth of understanding by city policy makers on this burgeoning sector within their boundaries. The impact, potential, and needs of these businesses are poorly understood.

The Urban Manufacturing Alliance conceived the State of Urban Manufacturing study as a way to fill this information gap and begin to give our members and other decision-makers information they can act on immediately in Baltimore, Cincinnati, Detroit, Milwaukee, Philadelphia, and Portland (Ore.). Longer term, we hope this information serves as a foundation to expand our understanding across the country. We have collected information directly from hundreds of manufacturers— including over 100 in Detroit—on the nature and challenges of their businesses; we also spoke with scores of Detroit-based organizations that support these firms.

Our goal is to begin to understand what the small-batch manufacturing sector looks like, who its entrepreneurs and employees are, and what cities can do to help these firms thrive and grow into larger jobs generators. We will release a snapshot of our findings for each of the six inaugural State of Urban Manufacturing cities, as well as a national report, that identifies promising practices that might be shared among cities to help these firms succeed. Finally, we hope the conversations we have had with businesses and stakeholders as part of this study have created relationships that will continue to grow the sector and the promise it holds for cities. To help ensure that, we have developed a “manufacturing ecosystem map” for each city that includes all of the organizations we worked with directly as part of the State of Urban Manufacturing process. There are other organizations that we haven’t yet worked with and we encourage Detroit stakeholders to continue to increase the coverage of this tool, which will help producers—and the organizations that support them—match the right resources to businesses’ needs or identify where gaps exist.

Methodology & Limitations

State of Urban Manufacturing was conducted in two phases, beginning in early 2016. Phase 1 helped us set the context across the country for urban manufacturing by analyzing publicly available data over a ten-year period (2004-2014) from 16 metropolitan areas. These metros represented a cross-section in terms of size, geographic region, and dominant manufacturing trends or “typologies” (i.e. metros seeing a growth in activity driven by one major industry; metros heavily focused on the innovation economy and advanced manufacturing; large metros with a diversified manufacturing base; smaller metros that are growing the fastest, both in terms of population and jobs; and metros with a strong artisanal / craft production sector). These included: Atlanta, Buffalo, Baltimore, Charlotte, Chicago, Cincinnati, Detroit, Houston, Los Angeles, Milwaukee, New York, Philadelphia, Portland (Ore.), Salt Lake City, San Francisco, and San Jose.

Focusing on the MSA level allowed for ease of comparison over time using easily obtainable data from the Bureau of Labor Statistics, Bureau of Economic Analysis, and U.S. Census, specifically observing manufacturing sector trends. The indicators we evaluated included: establishment change; employment change; wage rates and change; demographics of workforce; education of workforce; and contribution of the manufacturing sector to MSA-area Gross Domestic Product.

Figure 1: Detroit Metropolitan Statistical Area (MSA)

Because existing data reveal only so much about small-scale manufacturers’ challenges, we sought to understand with greater precision these businesses’ day-to-day experiences with the hope that it would spur new thinking about how service providers and advocacy groups can support these firms. In Phase 2, we used a survey to collect data directly from manufacturers in Baltimore, Cincinnati, Detroit, Milwaukee, Philadelphia, and Portland (Ore.). Questions focused on basic business demographics, challenges in scaling, and understanding where businesses go to get assistance and information when they need it. Where possible, we looked at how businesses in each city differed in the way they answered questions based on whether they were new or more established, big or small, or producing exclusively for themselves or others.

In each city, we also interviewed key policymakers and service providers—practitioners in economic development, community development, workforce development, real estate development, chambers of commerce, and neighborhood nonprofits. Finally, we conducted focus groups in each city with large manufacturers, small manufacturers, and the groups that support both with services like connections to financing, navigating regulations, market development, business acceleration, and finding affordable real estate.

While the State of Urban Manufacturing advances our understanding of this sector simply by providing perspective on what small-scale producers experience as they navigate business ownership and growth, our study has a few limitations worth pointing out.

The main limitation is that we did not develop a stratified sample in advance of our survey distribution and focus group recruitment, so participants are not necessarily representative of manufacturers as a whole in each city. In particular, we relied on community partners to promote the survey and focus groups, so participation in each place likely reflected the types of businesses our partners interact with most.

Introduction

Perhaps more than any other American city that rose to prominence in the 20th century, Detroit has manufacturing in its DNA. For three-quarters of the century it was the world’s center of production for the automobile—the machine that largely defined 20th-century America, and instigated shifts in global settlement patterns for at least 50 years. From the founding of Henry Ford’s eponymous firm in 1903, Detroit became not just the automotive capital of the world, but also a veritable R&D lab for mass production, engineering, and factory worker training and education. In addition to the headquarters of the big automakers, thousands of industrial suppliers still dot the southeast Michigan region—a testament to the dense hinterland of this production capital even as much of automotive and other large-scale production has shifted to other parts of America and overseas.

Despite that decline, Detroit has seen an emergence over the past several years of a burgeoning sector of small-batch and design-led production companies. This includes businesses like an internationally acclaimed denim apparel firm, a third-generation specialty metal fastener shop, and a variety of food and beverage producers. People comment on the hive of production activity occurring in Detroit today—and how much entrepreneurial spirit it is generating here and attracting from farther afield. Yet, this group of emerging entrepreneurs—and the various organizations and institutions that have sprung up to support them—is not particularly well understood. Their numbers are not apparent in the data collected by economic analysis agencies. And while they are often thought of as manufacturers, if smaller-scale ones, this does not always match these entrepreneurs’ own assessment of themselves. Many start out thinking of themselves as artists, artisans, or designers. That’s vitally important to understand because it may impact where these entrepreneurs go for assistance if they want to grow their businesses.

Indeed, our study shows that, despite Detroit’s strong industrial heritage, infrastructure, and a recent stabilization of production employment in the region, the city’s newer, smaller manufacturers face a variety of challenges to scaling. Business owners anxious to grow find it hard to hire aptly trained employees. There are millions of square feet of vacant industrial real estate in the region, but almost none of it is appropriate for small firms lacking capital to rehabilitate and subdivide those spaces. In fact, access to capital and appropriate space are two of the biggest challenges cited by the firms we surveyed and spoke to.

This is despite a collection of eager, motivated stakeholders—public and private alike—who have banded together in Detroit to help figure out what resources and services small-batch, design-led producers need access to in order to grow and thrive. The question for them is how Detroit can tune its industrial heritage and infrastructure to the needs of today’s—and tomorrow’s—manufacturers.

This is precisely what the stakeholders in Detroit wanted to understand better when they asked the Urban Manufacturing Alliance to include the city in its inaugural list of locations for the State of Urban Manufacturing study. We know that Detroit Creative Corridor Center, which is UMA’s designated community partner for the study, was speaking for many of its colleagues who support small-scale production in Detroit when they told us they wanted to know how these entrepreneurs contribute to Detroit’s economy, and what resources they need most to succeed and thrive.

Key findings we uncovered, discussed in detail below, include:

1. Small-scale manufacturers are struggling to get out of first gear, complementing their passion for their products with right-sized business know-how and technical support designed for established, but very small, businesses seeking to grow; as in many other cities, the preponderance of business support is geared toward startups or very large companies.

2. Despite immense tracts of vacant industrial space, there is a dearth of appropriate step-out space for businesses eager to graduate from operating out of their homes, incubators, or makerspaces, but who lack the ability to acquire, subdivide, and build out decrepit space.

3. This is indicative of a broader challenge of these businesses accessing capital at critical inflection points of their business trajectory—not just for new equipment or expanded space, but also the working capital needed to transition from the cash-on-the-barrelhead world of direct-to-consumer production to the world of 60- and 90-day terms of supplying wholesale markets.

4. Even though hundreds of thousands of highly skilled industrial workers and managerial experts remain in the region, Detroit’s small, growing businesses are having trouble finding and retaining skilled talent, leading to plateaus in businesses’ growth, and causing business owners to leave money on the table for orders they can’t fulfill.

5. Along these lines, southeast Michigan’s rich network of industrial suppliers and job shops could be a huge asset to designers looking to complement their greatest strengths with established production shops. Despite attempts to begin to catalog these important industrial assets, information is not organized in a way that helps small business owners new to manufacturing find the right, high-quality suppliers for their needs.

We’re pleased to share with you this snapshot of Detroit’s small-scale production economy, along with several recommendations that this motivated, highly active community might pursue to galvanize this movement in Detroit.

The Detroit Context

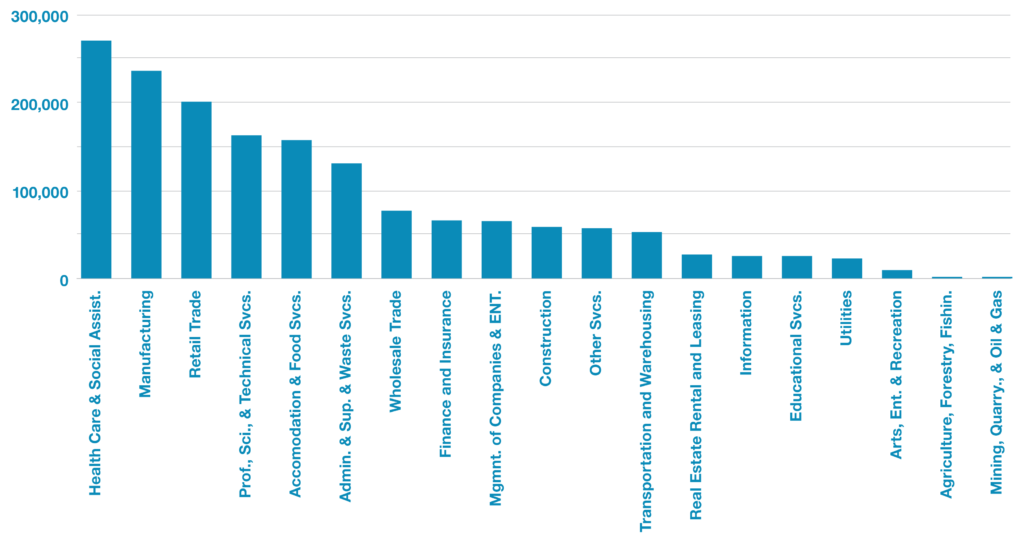

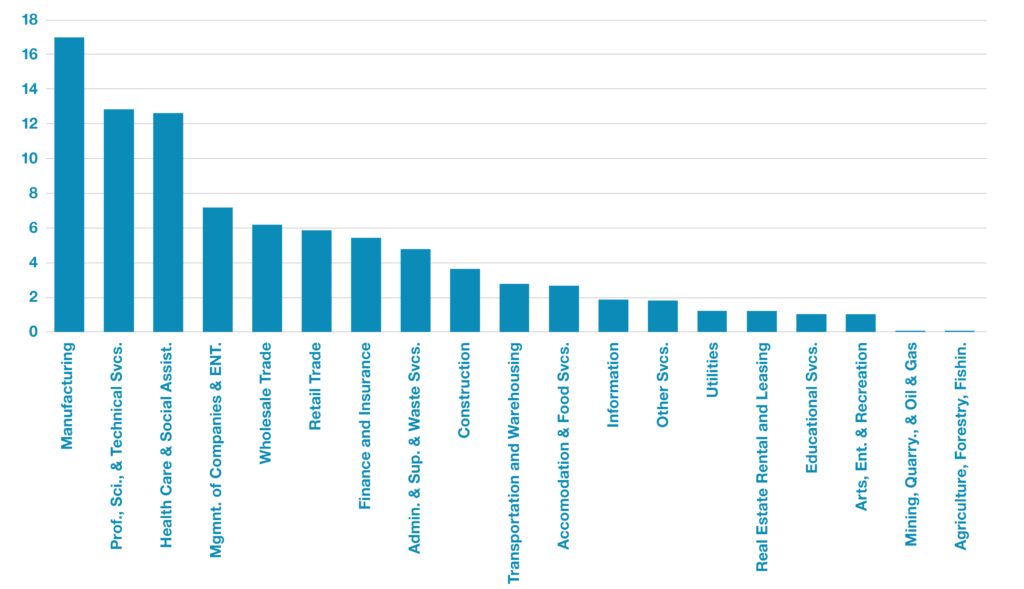

Detroit stands out among the six cities UMA studied in the State of Urban Manufacturing. Its region’s production workforce has stabilized recently after several years of decline. From 2010- 2015, the sector regained almost all of its job losses since the Great Recession, and, in 2015, employment was barely below its 2007 number. In 2014, manufacturing was the second-biggest employer with 236,072 jobs in the region (13 percent of the MSA total of 1,807,694). However, manufacturing had the highest total wages for the sector by a sizeable margin ($16.99 billion, or 17.3 percent of the MSA total).

Figure 2: Total Employment by Major NAICS Category

Figure 3: Total Annual Pay by Major NAICS Category (in Billion USD)

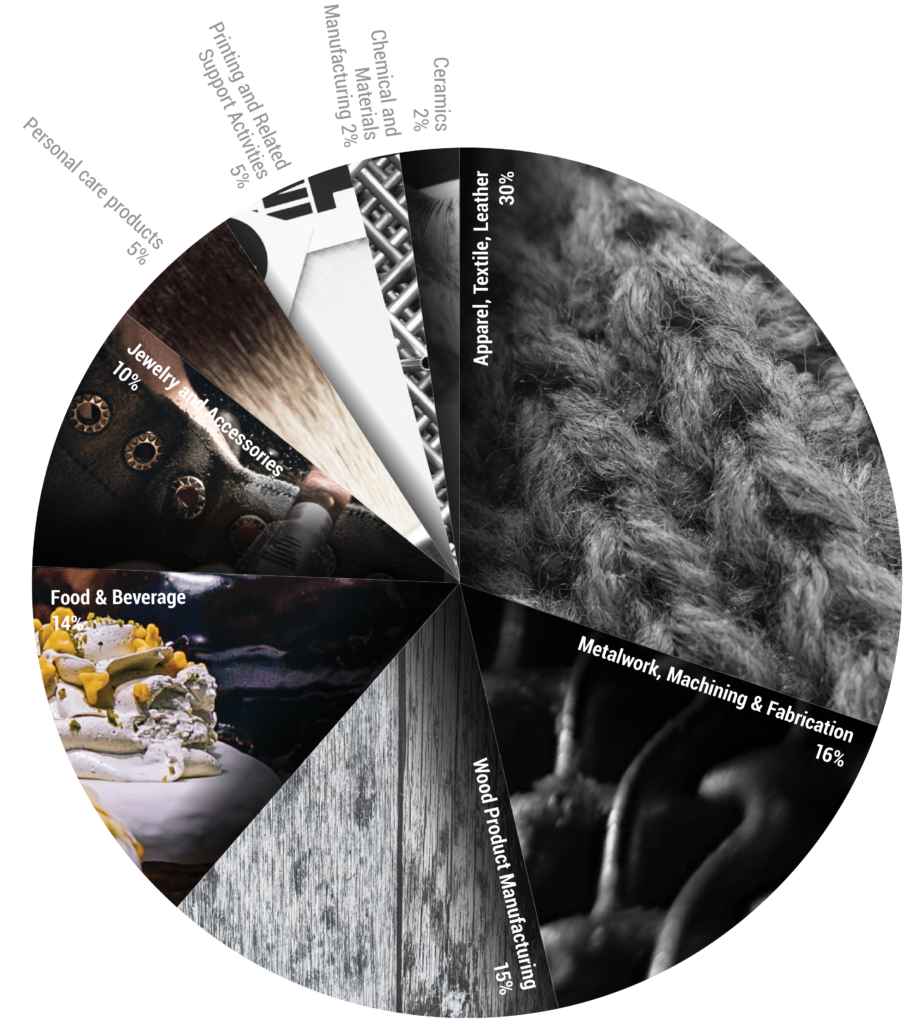

However, these numbers likely don’t capture the preponderance of the respondents to the State of Urban Manufacturing survey, which are more representative of the emerging maker and small-batch production economy. A total of 99 respondents completed our survey—a sample of the very firms that tend to fall through the cracks when data on traditional manufacturers is collected. Respondents’ businesses represented several sub-sectors, though the Apparel, Textiles, and Leather sub-sector responded twice as frequently as the next several.

Figure 4: Manufacturing Subsectors Among Survey Respodents (n = 99)

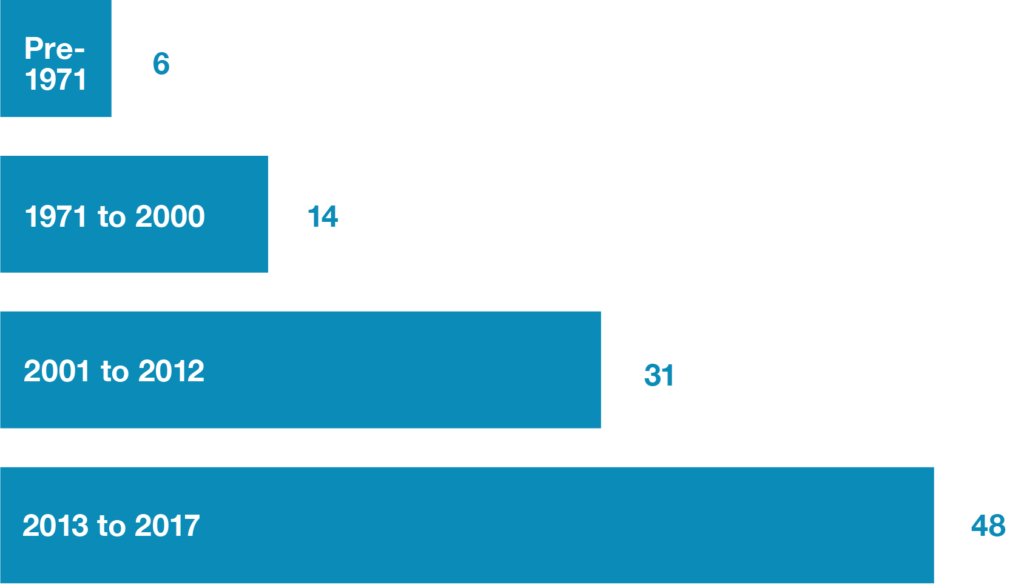

Businesses were relatively young; almost half were founded since 2013.

Figure 5: Year of Business Founding (n = 99)

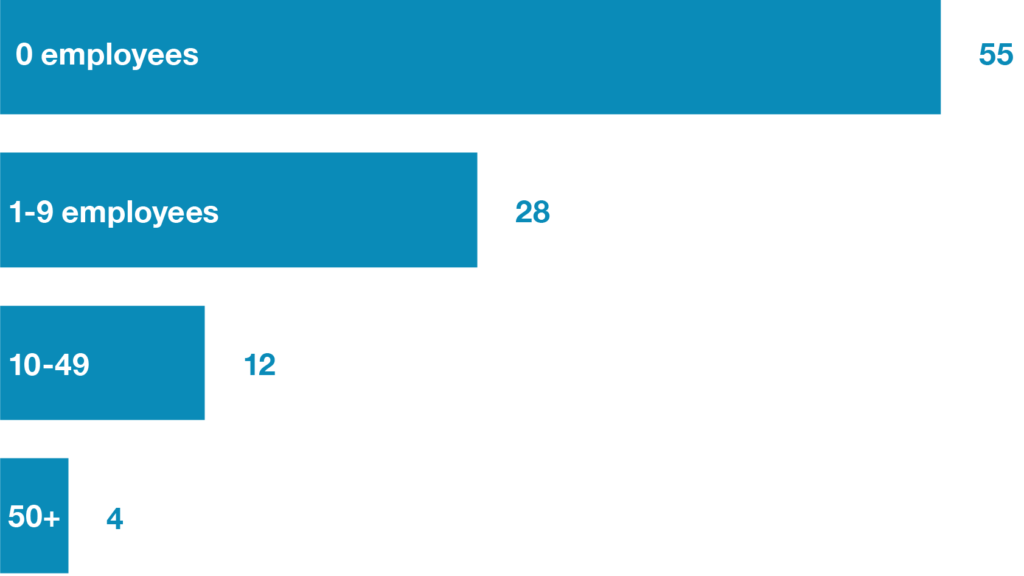

Figure 6: Number of Employees (n = 99)

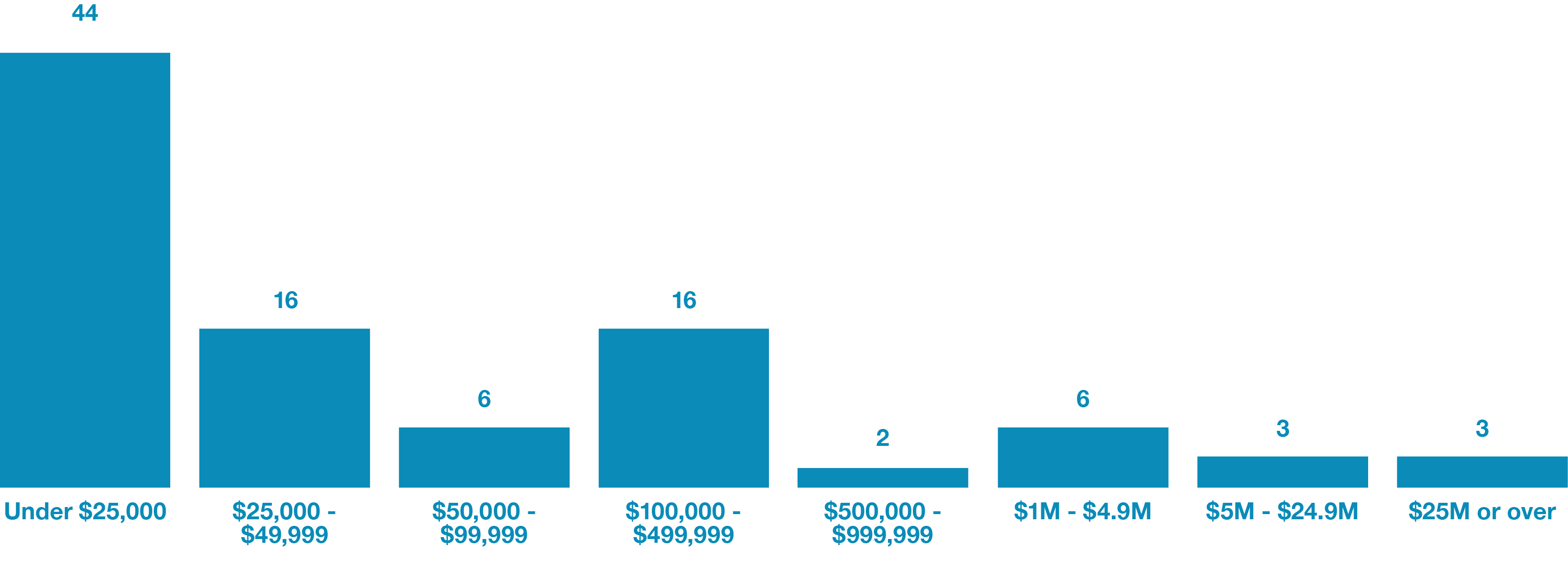

They were also quite small; 84 percent had fewer than 10 employees and more than half didn’t have any employees other than the owner. Among the 50 sole proprietorships, 38 percent of owners continued to hold other employment, an indication that the manufacturing business was not providing sufficient revenue to support the owner. Over 60 percent of the respondents reported 2016 sales of under $50,000 (almost half under $25,000).

Figure 7: 2016 Revenue (n = 96)

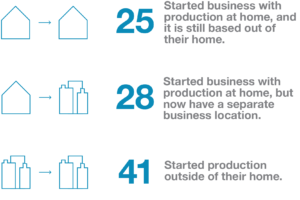

At the time of the survey, a quarter of respondents still operated their businesses from their homes. Nearly a third of firms reported that they had started their businesses in their homes but had “graduated” to separate business locations.

Figure 8: Business Location Over Time

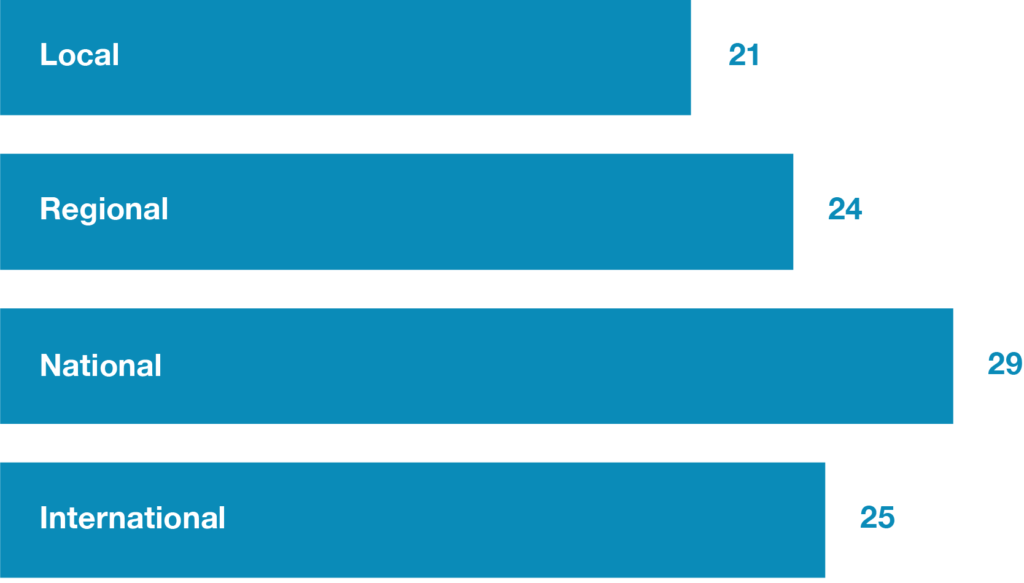

Despite their generally small size, over half of the respondents sell into national and international markets. And 82 percent experienced revenue growth in the previous year, with more than half reporting growth of 25 percent of more.

Figure 9: Broadest Market Reach Mentioned (n = 99)

There was also considerable appetite for future growth. An impressive 99 percent of respondents expect to have larger businesses in two years. Thirty-eight businesses plan to add employees over the next two years, and 66 said they would like to be in a larger space by then. Despite the appetite for growth, respondents pointed to several barriers to growth. Several of these lend themselves to key findings and recommendations which follow. We are sure that stakeholders will also find more that they will want to do in this regard.

Figure 10: Anticipated Space Needed for Next Location (Square Feet By Business) (n = 22)

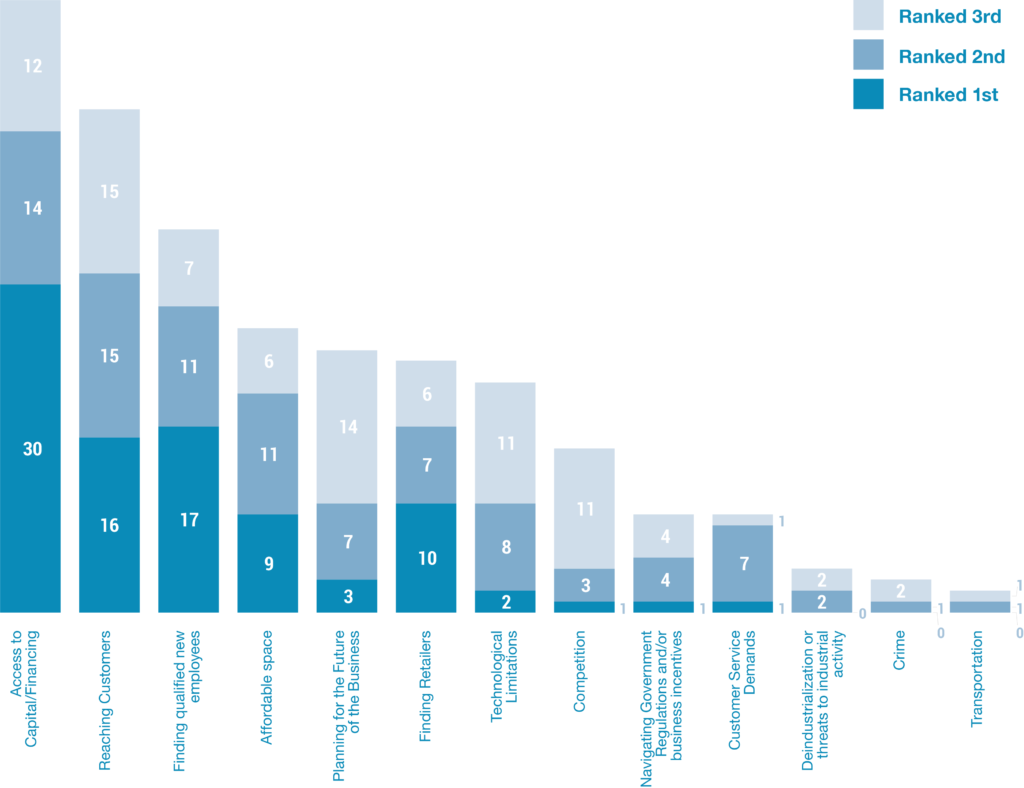

Figure 11: Barriers to Growth Ranked by Businesses

Key Findings

Business Support Services

It is clear from conversations and survey findings that most stakeholders see Detroit’s business support services as both plentiful and well-documented. (BizGrid was mentioned many times.) What’s less clear is whether the collection of services is robust enough in key ways to support businesses who have—or are about to—overcome the start-up hurdle and move into the next growth phase. Both business owners and service providers in our focus groups described the services offered as being tilted toward either entrepreneurs with business ideas looking to get started, or long-established firms able to navigate complicated incentive programs. There were relatively few services geared toward those in the middle looking to grow. (This tracks closely with other cities’ experiences.) This is a fundamental barrier to growth among a sample where half of firms were founded in owners’ homes, and half of those remain there.

Business owners in the throes of scaling up their businesses don’t have much time to research assistance or incentive programs, fully understand complex eligibility criteria, and then prepare applications—especially if they can’t be assured their applications will be successful. Business owners reported that the lack of a one-stop service provider made managing multiple relationships difficult. And the absence of an organization that acts as a case manager, helping to broker introductions and relationships for each business seems to mean that fewer growing businesses get connected with available specialty services they might need. But business support organizations reported that they felt stymied by an inability to share client information with other organizations freely as organizations respect client privacy or guard relationships that, in part, drive their own funding.

Maker-specific services were also reported to be lacking from the small business assistance ecosystem. “There are very few resources available about how you produce, manufacture, scale, distribute, arrange logistics, or handle day-to-day operations,” one service provider said. In addition, in spite of BizGrid, there is apparently “not a good directory of manufacturing [in particular] support services, especially among fashion and food producers, and contract manufacturers generally.”

Survey respondents also noted the challenge areas in which they would be most likely to seek help from external organizations. “Planning for the future” and overcoming “technology limitations” to growth were top items businesses would proactively seek information about from support organizations. It is clear that there is a forward-oriented, growth mindset to many of the businesses we heard from.

Photo Credit: Shinola

Access to Appropriate Growth Space in Detroit

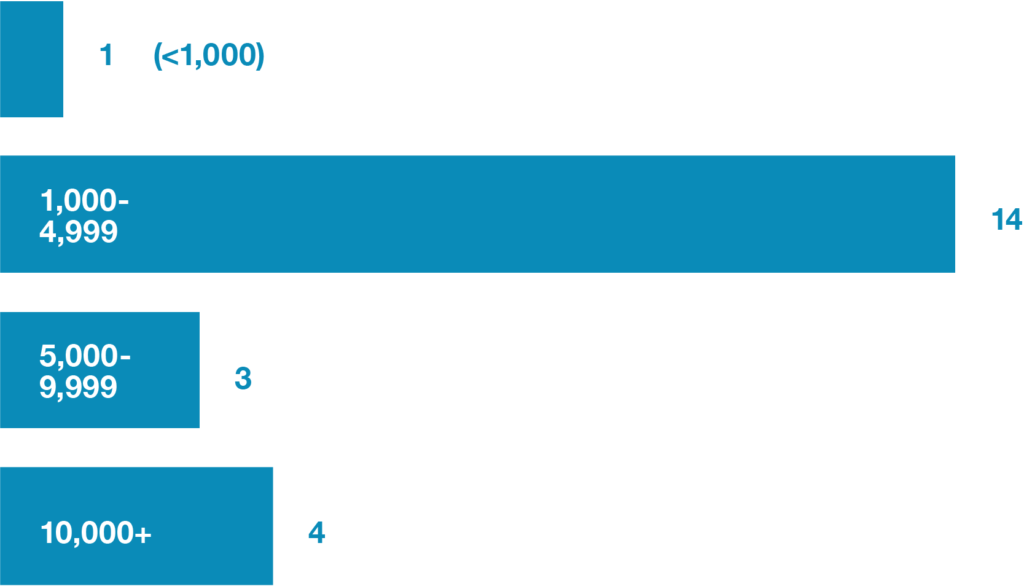

The data regarding the size of spaces that small businesses are moving into points to an important opportunity for Detroit. Inasmuch as survey respondents are representative of a wider population of micro-businesses that are scaling up, or on their way to doing so, an important component would seem to be an ample supply of relatively small, move-in ready spaces for them. But we learned from focus groups and conversations with other stakeholders that, despite an abundance of vacant industrial space in Detroit, the right kind of space—in good repair, clean, accessible, and subdivided—is in short supply. Significant investment is needed to bring most vacant space into a state of good repair, and to divide it into the sizes that scaling small businesses need most at a time in their growth trajectories that they are least likely to have available capital to do it themselves. Among those who indicated the desire to occupy more space, most envisioned expanding into spaces between 1,000 and 5,000 square feet.

Access to Capital

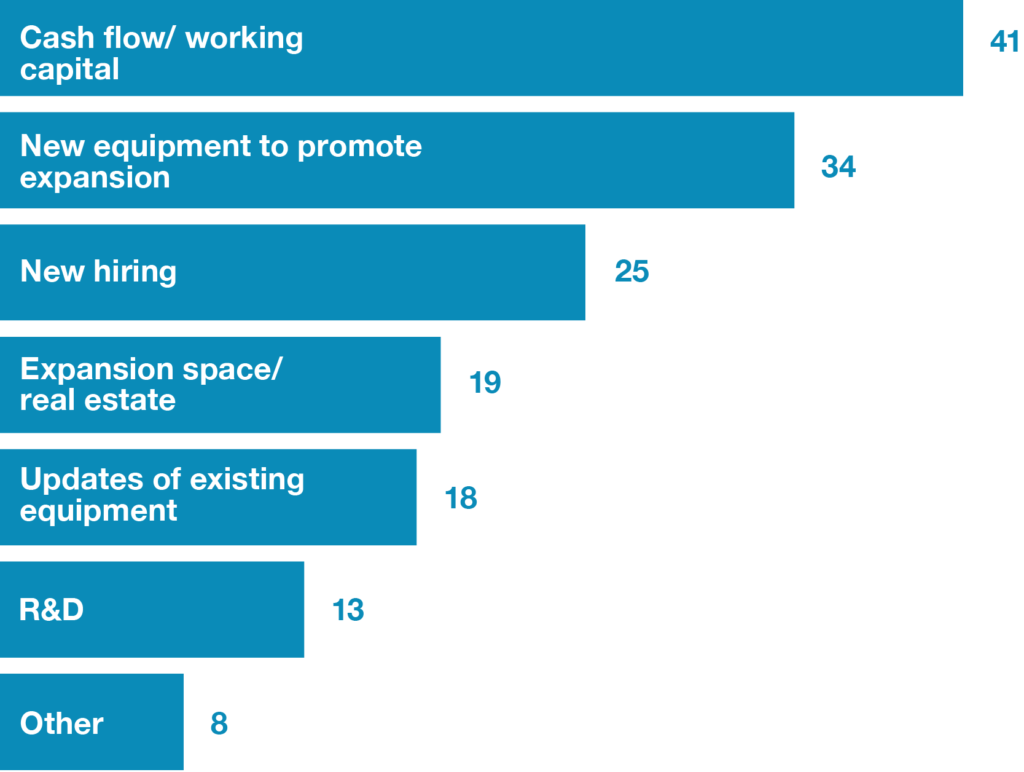

The chief challenge to expansion cited by Detroit respondents was access to capital. In addition to being mentioned almost twice as often as any other as a company’s most significant barrier, it received the highest number of mentions overall, cited as a top-3 barrier by 40 percent of respondents. A significant portion (43 percent) reported that they were either unsuccessful at obtaining financing or didn’t bother applying because they thought it would be too difficult for them to obtain. (This is a consistent pattern across the other cities we have surveyed and reinforces another message we heard consistently: that small business owners, who are pulled in too many directions, often will not apply for financing or other economic incentives if they aren’t assured of succeeding; the time and effort is too much to invest for an outcome that isn’t close to assured.)

More than three-quarters of 52 respondents who either had sought financing, or who would have done so if they had been confident in receiving it (and who answered a question on what they would have spent that financing on) indicated they needed it for cash flow or working capital, which are typically the hardest categories of financing for small businesses to land, given their limited business track records and lack of collateral.

It’s not surprising, then, that significant numbers of respondents reported using personal investment, personal lines or credit, or resources from family and friends as part of their start-up capital. However, when looking at who was taking advantage of each source of start-up capital, some notable findings emerged.

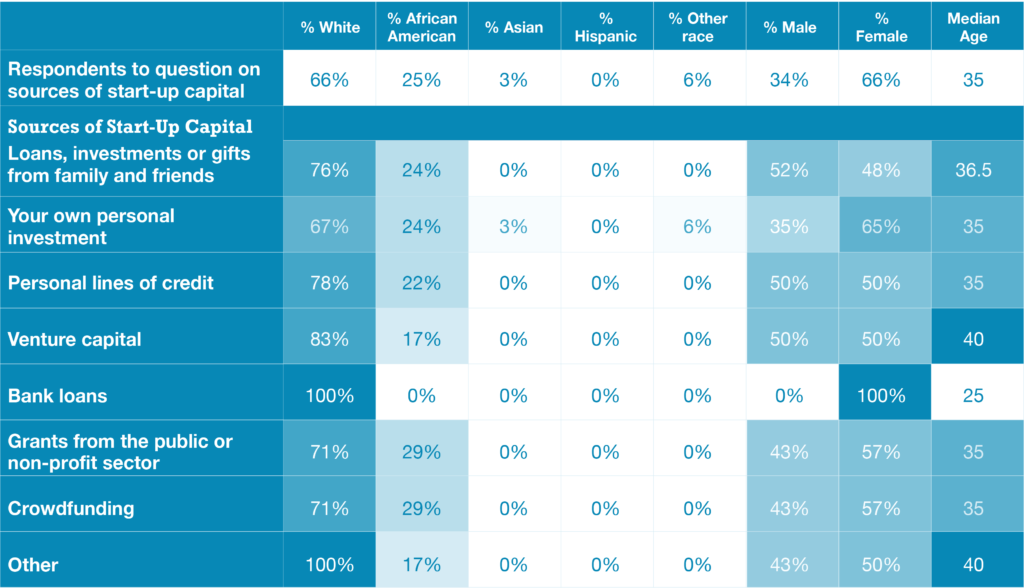

Figure 12: Sources of Capital Accessed, by Demographic Group

Compared to the sample who answered the question as a whole, those who identified as white over-represented among those who received bank loans, venture capital, and friends-and-family capital, and who used personal lines of credit. Those who identified as African American were under-represented among those accessing bank loans and venture capital. Indeed, no African American respondent to this question reported receiving a bank loan. Along gender lines, women were under-represented in all sources of capital except personal investment and bank loans.1

Focus group participants also echoed a familiar refrain: that finding financing for scaling manufacturing is tough because manufacturing feels like a risky bet for traditional lenders and it’s not sexy enough for angel investors and venture capitalists. One service provider to start-up manufacturers thought it might be worthwhile to try to grow a manufacturing-oriented angel and VC community, given Detroit’s manufacturing history. Another suggestion offered by focus group participants, which would be classified more as a workaround than as a solution to difficult financing, was to provide access to specialized equipment suppliers on a job-by-job basis, rather than asking a small producer to acquire such equipment for occasional use. Work would have to be done to identify the sorts of equipment that would fit into this category, and then to identify which suppliers could provide them.

Figure 13: Reasons Cited for Financing (n = 52)

Photo Credit: Detroit Denim

Hiring & Workforce Challenges

Respondents to UMA’s survey reported that finding qualified production employees was a significant barrier to their growth. Focus group discussions reinforced this. “I could make more money with more help,” one small producer said. “But I have to turn down wholesale orders because I can’t fulfill them” due to a lack of employees. Indeed, the Industrial Sewing and Innovation Center (ISAIC), a coalition of local sewn trades organizations and businesses, estimates that local apparel manufacturers lost between $2.6 million to $3.1 million in 2017 because of a lack of production capacity associated with insufficient access to a trained workforce.

Because production expertise, prototyping, and innovation are all built into Detroit’s workforce DNA, it’s surprising that finding skilled workers for growing firms is such a challenge. Have all of Detroit’s skilled tradespeople retired? Moved away? Are they looking for their former union-level wages that nascent firms are not in a position to pay? Participants wondered if there might be a way to partner with former workers to inform new workforce training curricula, before a generation of expertise is lost.2

In general, focus group participants also described the dearth of opportunities for young people to learn manufacturing trades. Secondary schools, in general, are not offering classes, although Macomb and Oakland Community Colleges (Romeo) were described as having made strides recently. In addition, Linked Learning was described as a new program creating opportunities for career pathways in engineering and advanced manufacturing by connecting high school career and technical education (CTE) programs to industry. There were also reported to be very few apprenticeships creating pathways and teaching basic fabrication skills—the understanding, for instance, of “feeds and speeds” associated with cutting metal of different gauges.

There was an almost universal sense that young people have been reluctant to pursue technical or vocational training. Manufacturing has been stigmatized as the most recent generation came to think of a college degree as the gold standard for gaining entry into the workforce.

Even when they do find either qualified or trainable staff to work on their production, several makers described being challenged by a constant churn of employees—working at a business for a short while and then leaving. Turnover like this is particularly challenging in a small shop where the business owner has made an investment to train an employee, and where there may not be sufficient capacity to cover work while a new employee is recruited.

A conundrum emerged during this part of the conversation—a flavor of which UMA has heard in most of the other State of Urban Manufacturing cities, too. Makers describe frustration among employees who have to engage in relatively repetitive work with near perfect attention to detail for long stretches of time. Yet, many of these makers describe their preference to hire individuals who, for instance, “are as passionate in my craft as I am,” as one maker in Detroit put it. This is perhaps endemic of any founder in start-up mode—the desire to find colleagues who internalize their ethos and approach to work. But it can lead to the challenge of finding staff willing to work at production wages but expected to exercise a high degree of creative thinking and self-direction, and able to apply independent thought and judgement during hours of repetitive tasks.

Another challenge is finding sufficiently skilled workers for small runs in very small businesses. In situations like these—which was the norm for some of the businesses we spoke with—there is often not sufficient work to employ a full-time artisan for more than several days or weeks at a time. One maker suggested an interesting approach to solving this problem: creating a shared workforce to be used among several makers. It’s a model that could work well with similar, but non-competing businesses. For instance, food packing/production for different products. Or health and beauty products, especially those made with food-grade materials and which are essentially another form of food production.

Contract Manufacturing

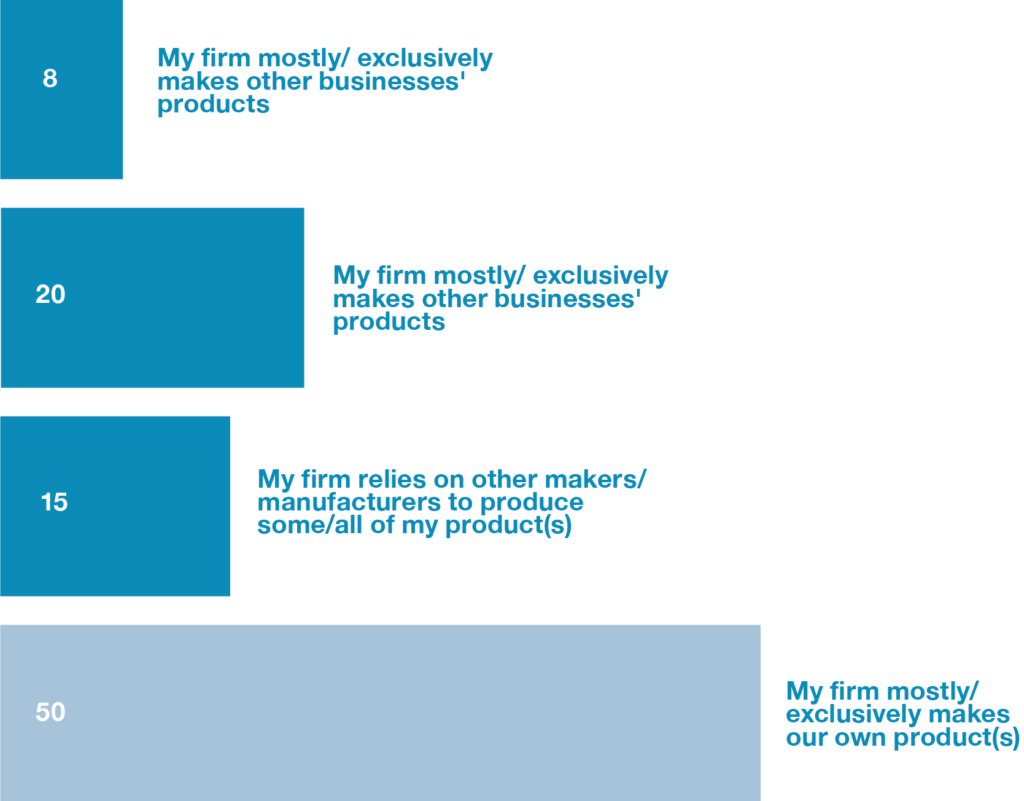

Surveyed businesses were asked if they either used, or served as, contract manufacturers. Among 93 firms answering this question, almost half engage in some level of contract manufacturing—either producing other businesses’ products, or contracting out the production of their own. About half of those that contract out do so to firms in Detroit or the surrounding region. More than a fifth take on contract work in addition to producing their own goods, which is a strategy many business owners use to help contribute to their bottom line. Cut-and-sew apparel manufacturers appear to be a big part of the contract manufacturing story in the survey sample, with several serving as contractors all or some of the time.

Figure 14: Firms That Engage in Contract Manufacturing (n = 94)

Many stakeholders have expressed their hopes of establishing better linkages between makers or designers and existing manufacturers, who might be sources of production capacity or coaching for them. Makers and designers might also be sources of new business for many established manufacturers, too.

Indeed, our study uncovered examples of this already happening among the responding businesses. “Our ideal scenario is NOT to scale our production in house,” said one small manufacturer. “We want to be small-batched, commission-based; we’d prefer using a third-party contractor to do large production runs.” And several write-in answers to a survey question on business challenges reflected companies’ interest in scaling their manufacturing through partnerships with contract manufacturers and others.

But more needs to be done, focus group participants said, to make this a realistic option for emerging designers, makers, and manufacturers.

The biggest impediment to fostering more of these relationships, they indicated, is simply in knowing what producers or suppliers exist throughout Southwest Michigan. “Many don’t have an online presence,” one focus group participant said. “And some barely have fax machines.” Others, it was anecdotally shared, are retiring or being bought out by larger customers and vertically integrated into their operations.

Participants indicated that a couple of entities have tried to pull together a directory—Pure Michigan Connect and D2D were both mentioned. But makers said those directories address only part of the problem. Suppliers oversell themselves in terms of competency, quality, and turn-around times; business owners seeking to use these suppliers are left having to do the work to figure it all out which are quality suppliers.

Survey responses also point to some challenges in increasing the number of contract manufacturing opportunities. Contract manufacturers were asked to identify challenges they experienced in working with businesses contracting work to them, selecting up to three challenges. The most commonly selected answers were “customer’s lack of preparation for production (design specs, materials)” and “customer’s lack of knowledge about pricing and cost.” This reinforces some of what we heard with respect to a dearth of services to help makers better understand production processes.

Employee Education & Demographics

Firms who indicated they had employees were asked about the demographics of their workforces. With respect to education levels—and contrary to the accessible way in which manufacturing jobs are often described—very few of the companies in our sample employed production workers with less than a high school diploma or GED. In fact, more than three-quarter reported that 90 percent or more of their production workforce has at least a high school credential, and more than a third reported that production workers possessed at least a bachelor’s degree were the majority of their production workforce.

Figure 15: Gender of Owner/Proprieter (n = 92)

Figure 16: Race of Owner/Proprieter (n = 89)

With respect to race, two of the four largest firms in the sample (by employment) had predominantly black production workforces—a stand-out among other State of Urban Manufacturing cities. Also notable, while other cities’ larger firms tended to be those with the more diverse workforces, 38 percent of firms in our sample in Detroit (excepting the four largest) had predominantly African American production workforces.

Finally, understanding that hiring practices can correlate with workforce diversity, we have examined how survey respondents conduct their recruitment. By far, the most common methods for production staff are referrals from friend networks (57 percent of firms reporting this method) or from existing employees (43 percent). Specific credentials and skills cited as desirable and/or difficult to find in job applicants included Serve-Safe certifications, experience in the skilled trades, and facility with the programming of CNC machines. Six companies (13 percent) explicitly mentioned that they consistently have trouble finding employees with sewing skills.

Photo Credit: Ali Lapetina

Business Owner Demographics & Definition

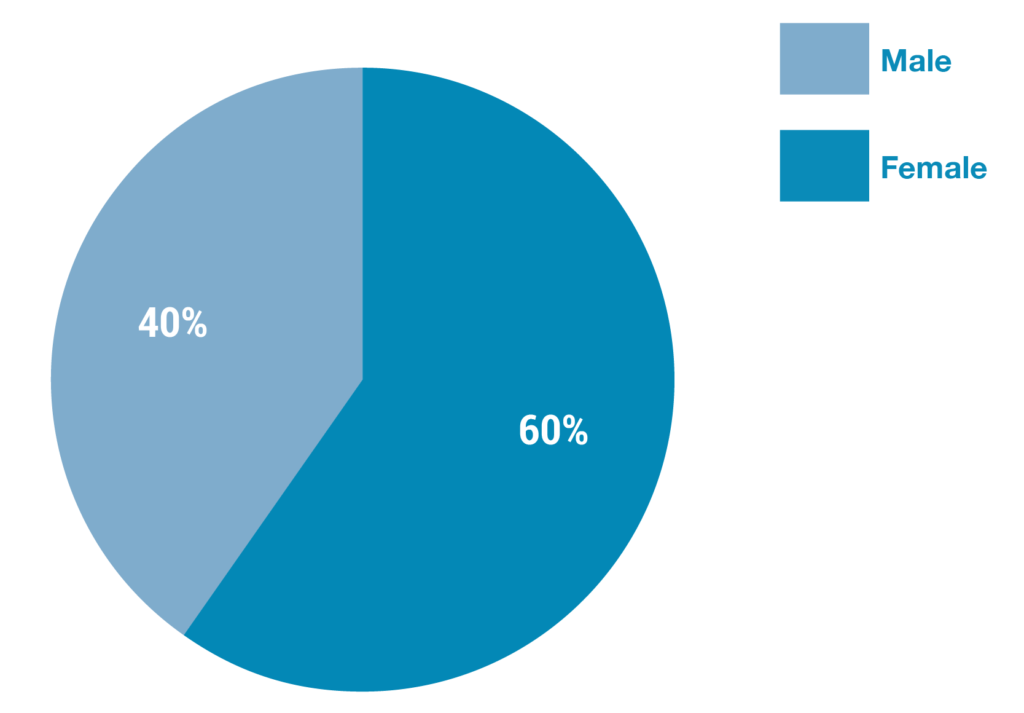

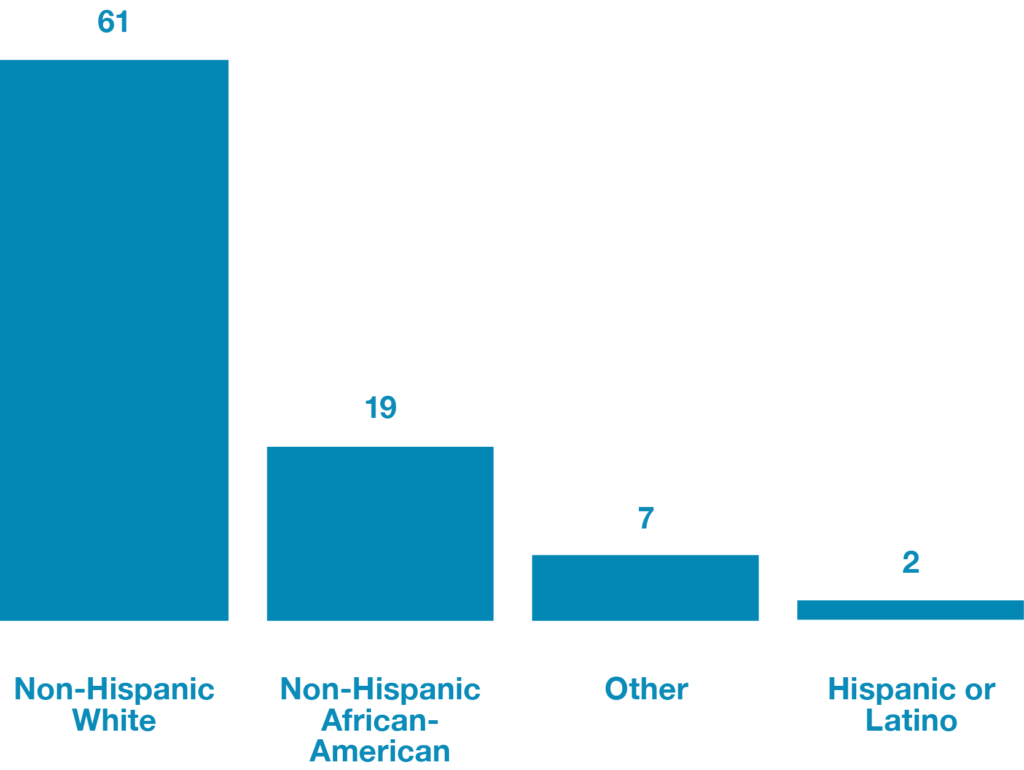

Of the business owners responding to the survey and identifying demographically, one in five was African American—the highest proportion of black respondents in any of the six cities UMA has examined as part of the State of Urban Manufacturing. Respondents were also more likely to be women (60 percent).

As in other State of Urban Manufacturing cities, respondents shifted their sense of themselves as owners from when they were founded to when they took the survey last year. More respondents thought of themselves as manufacturers, business people and entrepreneurs, and fewer described themselves as makers or artists.

Figure 17: Professional Identity of Principal/Owner Over Time

Recommendations & Opportunities

Right-size business support services to help businesses on their way to growth—not just the dreamers and the legacy firms.

Develop a slate of services that focus on micromakers who have overcome the start-up hurdle but need help as they begin to scale. You might begin by further surveying firms with nine or fewer people to more clearly document their needs and develop a slate of services particular for them. Firms that are earning between $100,000 and $1 million in revenue may be of particular interest from a policy perspective since they have overcome the start-up threshold and are well on their way to generating local job opportunities; they are also in the critical growth period where most owners struggle to shift from doing their business to running their business.

In addition, small-scale manufactures have consistently told us that the service providers they find most useful are the ones that don’t simply point them toward information, but help them to collate and synthesize the overlapping—often conflicting—details of the various programs that businesses can take advantage of with respect to hiring, real estate, tax abatements, and technical assistance.

One promising approach we identified is provided by Build Institute, which offers technical assistance to aspiring and current entrepreneurs. Build has graduated over 1,000 entrepreneurs from every corner of Detroit. Notably, their participants are 45% African American and 71% female. In addition, 85% of graduates are low- to moderate-income.

Tap a tiny fraction of Detroit’s vacant industrial space to create appropriate step-out space for growing businesses.

While additional analysis is needed to quantify the potential market for spaces in the 1,000- to 5,000-square foot range for growing makers, our study indicates the appetite is likely to be substantial. An appropriate stakeholder agency might undertake a market study to help private sector developers to warm up to the opportunity to create clean, flexible, move-in-ready space for makers—and to identify any subsidy that might be needed.

Help make capital available for growing businesses, when they need it most.

Consider developing a loan fund geared specifically to small-scale manufacturers that leverages lenders capital and business assistance groups’ expertise on producers’ particular needs. At the same time, work intensively with businesses on a growth trajectory to begin organizing their financial paperwork in advance of the point at which they will need to begin the underwriting review process.

NEIdeas is a program that celebrates existing businesses in Detroit, rewarding those with the best ideas for growth, through two competitive grant opportunities. One awards $10,000 to each of 20 businesses grossing less than $750,000 annually; the latter awards $100,000 to each of two businesses grossing between $750,000 and $5 million. (In addition, applicants who do not win a grant benefit by being welcomed into the NEIdeas network where they may access further opportunities in the entrepreneurial ecosystem. In 2017, over 20 percent of NEIdeas grantees were manufacturing-related.

There was also a suggestion among some in the business support community that a venture capital fund focused on small-scale manufacturers might be launched, given Detroit’s manufacturing heritage.

Finding skilled talent.

Several promising programs to build the production workforce were mentioned by business owners and stakeholders, and may be models to be expand upon or replicate. One is Linked Learning in Detroit, which combines rigorous academics, demanding technical education, personalized student supports, and real-world experience to high school students. Linked Learning provides college and career pathways organized around 21st century themes, including engineering and advanced manufacturing. Its programs have real-life experiences grounded in the skills that businesses have indicated are needed today, or will be needed tomorrow, ensuring the experience will lead to job-readiness after graduation.

One of the most intriguing ideas discussed was to explore creating a shared workforce that could be used among several makers—a model that might work well with similar, though non-competing, businesses. This could be handled by a trade organization or advocacy group working with a particular manufacturing subsector. This model might be tested in the sewn trades, which are already organizing in Detroit to create clear training and advancement pathways. Workers could be pooled among a half-dozen or more small firms with consistent, but not full-time, need for skilled staff. Another sector that might lend itself to a shared workforce is food and beverage production, serving as an interim step until businesses were large enough to invest in full-time staff, or to use an established co-packer. In both examples, the shared workforce could be administered by an organization also providing workforce-oriented wrap-around services that might better support jobseekers with higher barriers to entry and improve equity in the sector.

In addition, we heard several times that the region should attempt to tap its skilled industrial workforce before it disappears. It was nearly everyone’s sense that Detroit’s rich population of retired manufacturing workers and industrial engineers, with the right outreach, might be tapped as a corps of experienced professionals who could provide guidance to new and growing businesses. One focus group participant suggested it as “a maker-specific SCORE, maybe even based out of makerspaces to help recommend people to one another.”

Goals of increasing racial and gender diversity in the manufacturing sector were described by many business owners and stakeholders, including what steps could be taken to promote equitable access to available jobs in the sector for underrepresented groups. One important set of recommendations can be found in UMA’s, Pratt Center’s, and PolicyLink’s Prototyping Equity report.3

Tap the Detroit region’s rich network of industrial suppliers.

To help small makers scale, help connect them to established job shops capable of fabricating their products. To do this successfully:

- The region must better document vendors for contract manufacturing (for all or parts of processes). Perhaps more importantly, someone should take the lead in helping to make successful matches between current designers, small-batch producers, and

suppliers. (Local branding organizations do this effectively in other cities.) It is this handholding that makers say is most important

to them as they learn how to navigate the supplier ecosystem in their region. It is also the surest way to ensure that economic growth associated with the small-batch production sector stays local. - Help small businesses navigate the directory to understand which suppliers are of high quality and specialize in the particular aspects of a maker’s product; and

- Provide training for designers and makers on how to design their products for outsourced production, including: designing with production efficiency in mind, considering design approaches that take advantage of local production capabilities, and understanding how to convey designs in production specifications—something many contract manufacturers indicated was lacking among the makers they have worked with.

This is Just the Beginning…

This snapshot begins to shed light on the small-batch producers of Detroit, but it taps only a portion of the data collected. It is the intention of UMA that cities participating in the State of Urban Manufacturing study be able to take the full data set from the survey and focus groups and continue to pursue their own lines of inquiry. We hope each city will share additional findings as they become available so that the field of business support for small producers—including UMA and its members—may continue to benefit.

The Urban Manufacturing Alliance was generously supported by our National Title Sponsors, the Ewing Marion Kauffman Foundation and Bank of America Merrill Lynch, and our National Lead Sponsors, Google and Etsy. UMA would also like to thank Local Title Sponsor, Detroit Creative Corridor Center, and Local Lead Sponsors, Creative Many Michigan and Michigan Apparel Manufacturing, LLC.

![]()

Report authored Mark Foggin, and report design by Maria Klushina.

Acknowledgements

For their guidance on this research, thank you to Lee Wellington and Katy Stanton from the Urban Manufacturing Alliance; Laura Wolf-Powers, Ph.D., from the City University of New York Hunter College; and Olga Stella and Bonnie Fahoome from Detroit Creative Corridor Center. We received helpful support with data collection from many Detroit-based organizations, including Detroit Creative Corridor Center, TechTown, Build Institute, and Detroit Economic Growth Corporation. Thank you to Tanu Kumar and Jenifer Becker at Pratt Center for Community Development and Case Wyse at Pratt Institute’s Spatial Analysis and Visualization Initiative for their additional analysis of manufacturing data at the metropolitan level. Thank you to Adam Friedman at Pratt Center for Community Development and Greg Schrock, Ph.D., at Portland State University for their invaluable thought leadership throughout this process. Additional support for the State of Urban Manufacturing was provided by Emily Holloway from Hunter College; Johnny Magdaleno and Eva Pinkley from the Urban Manufacturing Alliance; and Cydney Camp from Detroit Creative Corridor Center. Most importantly, thank you to the survey respondents and focus group participants for their time and insights, without which this report would not have been possible.

Endnotes

1. Answers on capital access reflect the race of the survey respondent; in a small number of cases, it is possible that the individual responding to survey was not the business owner but, rather, a delegated representative in the company.

2. In the meantime, ISAIC is working with Goodwill Industries, Henry Ford Community College, and LEAR Corporation to connect local underserved communities with U.S. Department of Labor-certified apprenticeships that will feed into technologically- advanced apparel manufacturing jobs.

3. See more at: www.prattcenter.net/eie/strategies.